Watch Now

Listen Now

I’m thrilled to have Marlena Lee, Global Head of Investment Solutions at Dimensional Fund Advisors. In this role, Marlena leads a team dedicated to providing clients thought leadership, analysis, and education on a wide range of investment-related topics.

Marlena is a member of the Investment Research Committee and previously served as Co-Head of Research, helping shape the firm’s global research agenda by working with clients to identify topics of interest and overseeing the creation of research papers.

Prior to joining Dimensional, Marlena worked as a teaching assistant for Nobel laureate Eugene Fama, and earned a PhD in finance and an MBA from the Chicago Booth School of Business.

But the thing I love most about Marlena is how well she communicates complex ideas to broader audiences, so today I asked her to share a framework for evaluating popular investments and determining whether or not they belong in your portfolio.

Here are my notes from our conversation…

Sign up for my newsletter so you can easily reply to my emails with your thoughts or questions for the podcast:

Eugene Fama’s Contributions to Finance (00:40)

Marlena kicks things off by describing Eugene Fama’s legendary status in finance. Known as the father of modern finance, his groundbreaking work, especially on the efficient market hypothesis, has shaped the way investors approach the market. Marlena explains the core idea: market prices incorporate information so quickly that it’s nearly impossible to act on new information to gain an advantage.

This is the primary reason that traditional active management fails. (See: Why You Don’t Have to Pick Winning Stocks or The Failure of Active Management)

She also highlights Fama’s collaboration with Ken French, with their series of papers demonstrating that different parts of the market have different expected returns. This work laid the groundwork for factor investing. At the time their work on factor investing was published, terms used to describe different mutual fund strategies were more marketing than empirically sound. These days, it’s almost impossible to see a fund analysis that doesn’t use something like the Morningstar style boxes that distinguish between large-cap, small-cap, value, and growth—these are derived from their work.

My favorite part of this discussion is when Marlena shares a personal story from her time as a student of Gene. Professor Fama has a notoriously tough teaching style. Marlena recalls repeatedly raising her hand to answer a question incorrectly, thinking that maybe she just didn’t word it correctly. After her third attempt to convey the same answer in different words, Fama told her to “go stand in the corner.” She laughs as she tells the story because, despite the embarrassment, she persisted and eventually became his teaching assistant.

Evaluating Investment Fads (06:39)

In my opinion, both individual investors and financial advisors struggle with how to evaluate whether a new investment idea belongs in your portfolio, especially when certain investments seem to be on everyone’s radar. Marlena introduces a framework for evaluating whether something is a good addition to your portfolio or simply a fad that can be ignored.

The first step, as Marlena puts it, is defining what a fad actually is. She describes it simply as “the dumb things we do because everyone else is doing them.” That really struck a chord with me, because we’ve all seen fads come and go, not just in investing but in fashion, health, and so many other areas. What makes investing different is that fads can do real damage to your long-term financial goals if they’re not approached with caution.

The cornerstone of Marlena’s framework is asking a simple but critical question: Why do you expect this investment to have a positive return? This question forces you to step back and consider whether the investment is grounded in solid economic fundamentals or if it’s being driven purely by speculation or excitement. She draws a clear distinction between productive assets (like stocks and bonds) and speculative ones (like gold or cryptocurrency).

Here’s how she explains it: Stocks and bonds are tied to real economic activity. Companies raise capital to invest in projects, produce goods, and drive economic growth. This activity generates future cash flows, which provide the foundation for positive returns. That’s why we can reasonably expect stocks and bonds to deliver over time—they’re contributing to the economy.

On the other hand, speculative assets like gold or cryptocurrencies don’t have this same mechanism. They don’t generate cash flows or produce anything of real value. Their price movements are largely based on the belief that someone else will be willing to pay more for them in the future, rather than being tied to any inherent productive capacity. Marlena makes a strong case that while these assets may have moments of explosive growth, they lack the long-term potential that stocks and bonds offer because they don’t drive economic growth.

She emphasizes that if you can’t clearly answer the question of why an investment should generate positive returns, it probably doesn’t belong in a well-diversified, long-term portfolio.

Marlena also reminds us that just because something has performed well in the past doesn’t mean it will continue to do so. This ties into her caution against extrapolating past returns, which is one of the most common mistakes investors make. She warns that investors often get caught up in the fear of missing out (FOMO) when they see others making money on an investment trend, but chasing recent performance usually leads to disappointment in the long run.

Investing is a long-term game that should be boring. The most exciting investment ideas are often the ones that are the riskiest. If an investment feels “hot,” that’s probably a signal that it doesn’t belong in a portfolio designed for long-term goals. Instead, you should be focusing on building a diversified portfolio with productive assets that generate real economic value over time.

Scarcity, Growth Stocks, and Extrapolating Returns (11:10)

But what about a company like Amazon? Here’s a company that clearly contributes to the economy, but does its dominance make it a safe bet for long-term investors?

Marlena uses this as the perfect example to introduce the next part of her framework, which focuses on the common mistake of extrapolating past returns into the future. Amazon is a growth stock, and as Marlena explains, its high price reflects not just the company’s strong performance but also investors’ lofty expectations for future growth. However, there’s a catch: this also means that the perceived risk of Amazon is lower, which means that the return investors should demand/expect should be lower too.

The more a stock’s price rises, the lower its expected returns become. While companies like Amazon have delivered incredible returns in the past, that doesn’t guarantee similar results in the future. As stock prices increase, they often become more expensive, meaning that future returns are likely to diminish.

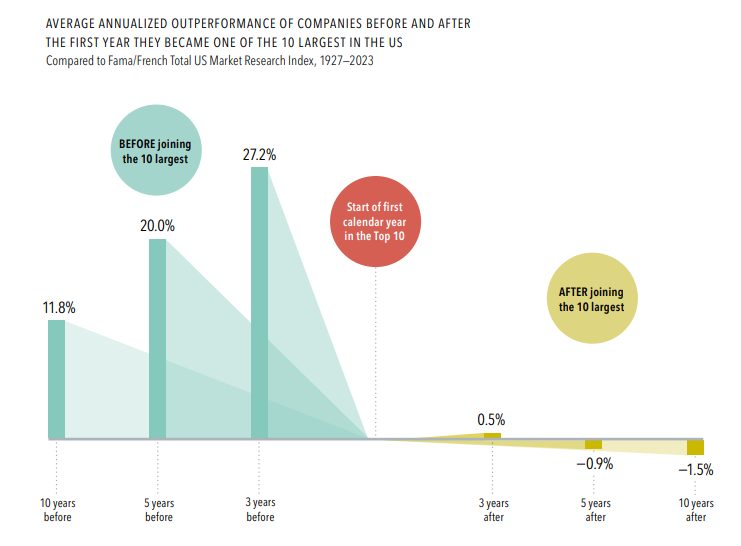

Consider the chart below that details research from Dimensional. Once companies make it into the top 10 largest U.S. firms, their performance tends to plateau or even underperform the broader market. Investors often assume that the biggest, most well-known companies will continue to lead the pack, but history tells a different story. The market tends to reward risk, and the largest, most established companies often carry less of it, leading to lower potential returns in the future.

Source: Dimensional Fund Advisors

She also ties this concept into the idea of scarcity, particularly when it comes to assets like gold or cryptocurrencies, which are often touted for their limited supply. While scarcity can play a role in driving prices higher, it doesn’t automatically translate to long-term returns. Just because something is scarce doesn’t mean it’s productive. Amazon may be dominant, and Bitcoin may be scarce, but that doesn’t mean they will continue to generate outsized returns going forward.

The key takeaway here is that you can’t rely on past performance or market dominance as an indicator of future success. If anything, high past returns can be a signal that future returns will be lower. Marlena’s advice is to avoid chasing what’s already hot and instead focus on a disciplined, diversified investment strategy that doesn’t hinge on a single company or trend.

The Importance of Global Diversification (14:13)

Marlena reinforces what I’ve often stressed on the podcast: putting too much focus on U.S. stocks, especially on the tech giants that dominate the market, is risky.

The “MAG Seven” (Amazon, Apple, Alphabet, Meta, Microsoft, Nvidia, and Tesla) have become so large that they now make up over a third of the S&P 500’s total value. What’s even more striking is that these seven companies now have a combined market weight equal to the next seven largest non-U.S. countries—combined!

See More: Is the S&P 500 Too Concentrated?

While it’s tempting to pile into what’s been performing well, Marlena explains that high market concentration can be a warning sign, not just in terms of risk, but also in terms of future returns. Historically, U.S. stocks have not always been the top performers. Marlena reminds us of the period following the dot-com bust, when U.S. stocks underperformed international markets for years.

See More: Are US Stocks Enough for Your Portfolio?

She also emphasizes that the current high valuations in the U.S. suggest that future returns for U.S. stocks may be lower compared to global markets. With U.S. stock prices near historical highs, this is an ideal time to consider adding more global exposure to portfolios.

Diversification is often called “the only free lunch in investing,” and today’s market conditions make global diversification more essential than ever. Whether you’re chasing growth stocks or concerned about missing out on U.S. market returns, the data and history show that maintaining a globally diversified portfolio is one of the most effective ways to protect against market volatility and maximize long-term gains.

Gold and Cryptocurrencies as Investments (29:46)

Gold has been viewed as a “safe haven” for centuries. People are drawn to gold because it’s tangible, scarce, and historically used as a store of value. But while gold might feel like a stable asset, it doesn’t produce anything—it just sits there.

Unlike stocks or bonds, which generate cash flows and contribute to economic activity, gold doesn’t have a mechanism for delivering long-term returns. Its value is largely based on the belief that it will remain valuable in times of crisis, but as an investment, it offers little beyond its scarcity and historical legacy. In essence, holding gold comes with an opportunity cost—you’re giving up the potential returns you could get from assets that are actually working to generate value over time.

Marlena emphasizes that while gold can have its place in certain scenarios, particularly for those who are deeply worried about doomsday-type events, it’s not an efficient part of a well-diversified portfolio. Even in times of economic uncertainty, other asset classes, like bonds, can offer stability without the downside of gold’s lack of returns.

For most investors, the peace of mind that gold offers doesn’t justify the potential loss in long-term growth. As Marlena puts it, if you’re investing in gold because you expect it to perform like stocks or bonds, you’re likely going to be disappointed.

Crypto enthusiasts often argue that Bitcoin and other cryptocurrencies are the “new gold,” offering a digital form of scarcity in a world that’s increasingly moving away from physical assets. But Marlena is quick to point out that, much like gold, cryptocurrencies don’t produce anything of value. They don’t generate earnings or contribute to economic growth. In fact, cryptocurrencies are even more volatile than gold, and their prices can fluctuate wildly in short periods of time.

She also highlights an important distinction: while gold has been around for thousands of years and has a proven track record of holding value in times of crisis, cryptocurrencies are still in their infancy. The technology behind them is evolving, and the regulatory environment is uncertain. That makes crypto far riskier than gold, and Marlena questions whether cryptocurrencies really belong in a long-term portfolio at all.

Unlike productive assets such as stocks and bonds, there’s no clear mechanism for cryptocurrencies to generate returns over the long term. Their value is driven almost entirely by speculation—by the hope that someone else will pay more for them down the line.

Marlena also addresses the argument that Bitcoin and other cryptocurrencies are scarce, with limited supplies built into their design. But as she points out, scarcity alone doesn’t create value. Just because an asset is hard to come by doesn’t mean it will generate returns. You can apply this logic to things like baseball cards or rare collectibles—while they might be valuable to some, their worth is entirely dependent on demand from others rather than any intrinsic ability to produce value. Cryptocurrencies, despite their scarcity, fall into the same category.

See More: Bitcoin ETFs Are Here, Should You Invest? and 7 Things To Know Before You Invest in Bitcoin

Marlena is also skeptical of cryptocurrencies as a hedge against inflation or as an alternative to traditional currencies. Cryptocurrencies are still extremely volatile, making them poor stores of value in the way that traditional currencies or even gold are. Their wild price swings make it difficult for them to function as reliable hedges or currencies in any meaningful sense.

She also takes the opportunity to address a common argument for both gold and cryptocurrencies—that they provide diversification benefits because they are often uncorrelated with stocks and bonds. While it’s true that these assets may have low correlations with traditional investments, Marlena warns that this alone isn’t a reason it will improve your portfolio’s overall risk-return profile.

Marlena’s advice is to think critically about why you want to include these assets in your portfolio. If it’s purely for diversification, there are better, more productive ways to achieve that through bonds, international equities, or other traditional investments. Diversification shouldn’t come at the cost of expected returns, and gold or cryptocurrencies often fall short in this regard.

Hedge Funds and Private Investments (36:36)

The final portion of our conversation focuses on hedge funds and private investments. These types of investments often seem like a good way to enhance returns or diversify a portfolio, but as Marlena explains, they come with significant risks and complexities that many investors may not fully appreciate.

Hedge funds are often seen as sophisticated investments reserved for high-net-worth individuals and institutions, promising outsized returns and unique strategies that can supposedly outperform the market. However, Marlena is quick to point out that hedge funds, while complex and often high-cost, don’t always deliver on these promises. In fact, she highlights that hedge funds typically invest in the same kinds of assets that are available in public markets—stocks, bonds, and other securities—but with much higher fees and a lot more leverage.

She also emphasizes that the data doesn’t paint a flattering picture of hedge fund performance. Over time, very few hedge funds can consistently beat the market. In fact, studies have shown that only a tiny percentage of active managers, including hedge fund managers, are able to outperform their benchmarks over long periods of time. Marlena mentions that just 17% of active managers who were in business 20 years ago are still around and have beaten their benchmarks.

Private investments such as private equity, private credit, and private real estate seem appealing because they tap into a different part of the market, providing exposure to companies that are in earlier stages of development or that operate outside of the traditional public markets.

At first glance, private investments can seem like a great way to diversify beyond traditional stocks and bonds. But one of the main differences between private investments and public markets is concentration risk. Marlena points out that when you invest in a globally diversified stock and bond portfolio, you might be exposed to thousands of companies across different sectors and regions. But with private investments, you’re often investing in a much smaller number of companies—sometimes just a handful. This lack of diversification can amplify risk.

Moreover, the returns in private investments can vary dramatically depending on the manager’s skill. Marlena emphasizes that manager selection is absolutely crucial in the private investment space. The range of outcomes for private investments is much wider than for public markets because the investments themselves are often more concentrated and less liquid. A skilled manager can generate strong returns, but an average or below-average manager could significantly underperform, especially after factoring in the higher fees associated with private investments.

This leads to another critical point—access. Marlena reminds us that while top-tier private equity managers can deliver strong returns, they’re not always accessible to the average investor. Many high-performing private investment funds are only available to institutional investors or ultra-high-net-worth individuals. For the average investor, gaining access to these top-tier funds can be difficult, leaving them with less proven or less experienced managers.

Private investments also come with significant liquidity constraints. Unlike public stocks and bonds, which can be bought and sold quickly and easily, private investments are often locked up for years. This lack of liquidity means that investors can’t easily access their money if they need it, and they’re often tied to the performance of a small number of investments for a long period of time. Marlena points out that for investors who value flexibility and the ability to rebalance their portfolios, this illiquidity can be a major drawback.

Another factor to consider is the lack of reliable data on private investments. Public companies are required to report earnings, disclose financials, and are subject to regulatory scrutiny, giving investors a wealth of information to make informed decisions. In contrast, private investments are much less transparent.

With private investments, getting accurate data on their performance can be challenging, and the benchmarks used to compare private investments to public markets are often not clear-cut. Without clear data, it’s difficult to assess whether a private investment is truly adding value to a portfolio.

Marlena sums it up well: while private investments can offer some diversification benefits, they also introduce a host of new risks, including concentration risk, liquidity issues, and the challenge of finding skilled managers. For most investors, the decision to include private investments in a portfolio should come down to whether they can tolerate these risks and whether the potential for higher returns justifies the added complexity.

Resources:

- Why You Don’t Have to Pick Winning Stocks

- The Failure of Active Management

- Is the S&P 500 Too Concentrated?

- Are US Stocks Enough for Your Portfolio?

- Bitcoin ETFs Are Here, Should You Invest?

- 7 Things To Know Before You Invest in Bitcoin

The Long Term Investor audio is edited by the team at The Podcast Consultant

Submit Your Question For the Podcast

Do you have a financial or investing question you want answered? Submit your question through the “Ask Me Anything” form at the bottom of my podcast page.

Support the Show

Thank you for being a listener to The Long Term Investor Podcast. If you’d like to help spread the word and help other listeners find the show, please click here to leave a review.

I read every single one and appreciate you taking the time to let me know what you think.

Free Financial Assessment

Do you want to make smart decisions with your money? Discover your biggest opportunities in just a few questions with my Financial Wellness Assessment.