Listen Now

In the realm of investing, there may not be anything more seductive than picking a winning stock. And not just a stock that goes up, but one that doubles time and again.

In my opinion, one of the reasons people buy individual stocks is the dream of finding that stock, and the psychology around it is somewhat similar to the psychology of buying lottery tickets.

The very dangerous difference, however, is that people know they are going to lose when they buy a lottery ticket. Stocks, on the other hand, provide a far greater sense of control over our own destiny.

See: Should You Invest in Individual Stocks?

Unfortunately, that’s simply an illusion, and one that financial media and even the brokerage apps and websites seek to enforce. In reality, investing in individual stocks is quite risky and (as I’ll explain in this episode) not even necessary.

Sign up for my newsletter so you can easily reply to my emails with your thoughts or questions for the podcast:

A History of Individual Stock Returns

Numerous studies provide compelling evidence that the majority of individual stocks fail to outperform the broader market, and even risk-free assets, over their lifetimes.

One notable example is from Hendrick Bessimbinder, titled: Do Stocks Outperform Treasury Bills?

In this paper, Bessembinder analyzes the total returns of U.S. common stocks from 1926 to 2016 in which he finds that the median stock generated a return of -3.66% per year, and only 42.6% of individual stocks had lifetime returns that exceeded those of one-month Treasury bills.

Meanwhile, the top 4% of stocks (1,092 out of 25,967) accounted for all the net wealth creation during that period, with only 90 companies (0.33%) accounting for more than half of the return.

A more recent example comes from J.P. Morgan’s Agony and Ecstasy, which finds that 66% of all stocks trail the Russell 3000 from 1980-2020.

Goldman Sachs research from 1986-2022 shows the median stock in the Russell 3000 had a 31% chance of losing more than 30% of its value in one year compared to just a 5% chance for the Russell 3000 index. Even more, 36% of Russell 3000 stocks suffered a permanent impairment defined as a stock that loses more than 75% of its value and does not recover to 50% of its original value.

These findings highlight the risks of relying on individual stocks. The significant skewness in returns means the likelihood of any given individual stock beating the market is quite low.

If this doesn’t resonate with you, then consider the performance of professional stock pickers.

The Failure of Active Management

Since first published in 2002, the S&P Indices Versus Active (SPIVA) Scorecard has served as a de facto measure of the effectiveness of active management versus indexing.

The SPIVA scorecard is released twice a year. Here is the most recent version as of this recording, which shows more than 79% of all U.S. Equity Funds trailed their respective benchmarks over the last 3-year period, 85% failed over the last 5-years, and more than 91% failed over the last 10-, 15-, and 20-year periods.

Global, International, and Emerging Market Funds didn’t fare much better, failing to beat their benchmark roughly 70-95% of the time depending on the time period measured.

| Fund Category | 1-Year | 3-Year | 5-Year | 10-Year | 20-Year |

| All Domestic Funds | 75.32% | 78.97% | 84.82% | 91.44% | 93.97% |

| Global Funds | 73.60% | 87.93% | 83.33% | 90.95% | 91.27% |

| International Funds | 68.07% | 69.98% | 77.97% | 87.80% | 93.38% |

| Emerging Market Funds | 63.30% | 73.50% | 74.67% | 89.20% | 95.24% |

These results are not unique to this specific report or point in history. You can Google past years of the SPIVA report and find similar results. Obviously the numbers vary a bit year-to-year, but the one trend that seems to always stay intact is that underperformance rates rise as the time period being measured lengthens.

So here’s what we know:

- Individual stocks are very risky and the probability that you can even match the overall market’s return buying individual stocks is very low.

- Professional investors running actively managed funds struggle with security selection, too.

Here’s the good news: you don’t have to pick winning stocks to earn the returns you need to reach your goals.

The Best Performing Stocks

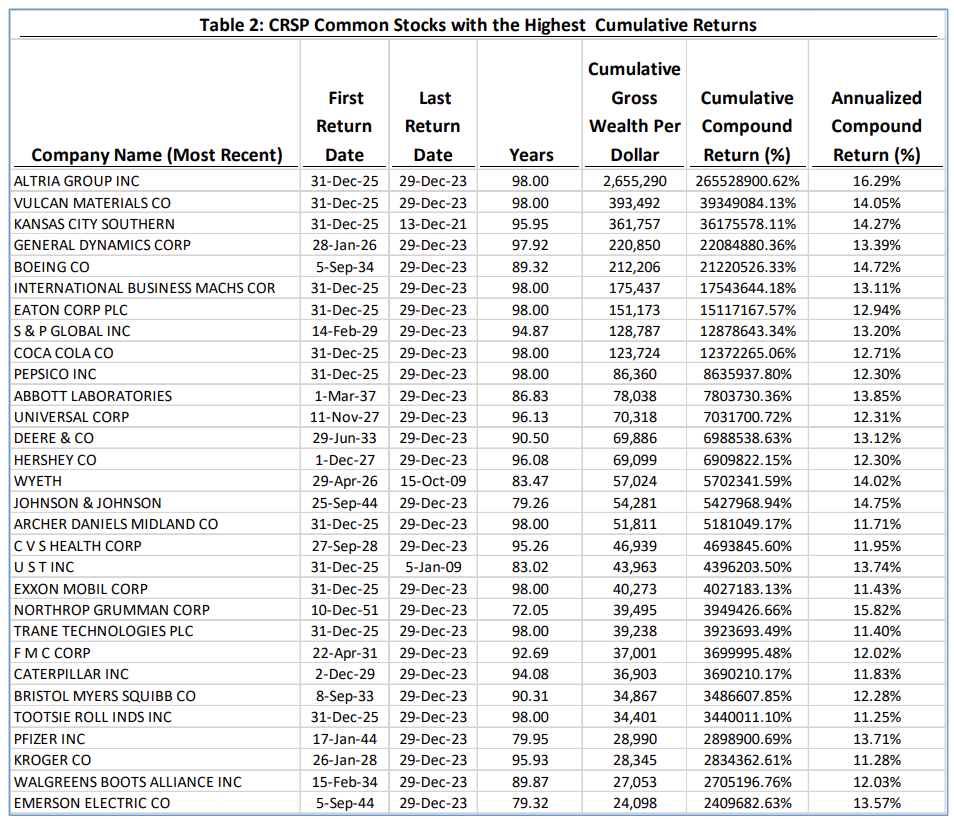

There’s a new paper by Hendrik Bessembinder has been making rounds that identifies the highest long-term returns among common stocks dating back to December 1925.

Since hitting it big on an individual stock is the ultimate investor pipedream. Let’s start with the winners. Below is a chart from the paper that highlights the common stocks with the highest cumulative returns.

Most investors will recognize many, if not all, of the best performing companies going back to 1926 because they are largely what would be considered blue chip stocks today.

Perhaps the most shocking result is the difference between the mean (average) cumulative return and the median (midpoint) cumulative return. Going back to 1926, the average cumulative return was 22840% while the median cumulative return was -7.41%.

Now here’s the good news…

If you’re broadly diversified and own something like a total US stock market index, you own and benefit from any given stock that delivers outsized returns.

Proponents of diversification, including myself, often highlight benefits of diversification such as preventing a catastrophic loss in one investment that materially impacts your overall portfolio. But the other benefit of broad diversification, particularly when you own the entire market, is that you effectively guarantee that you won’t miss out on the winners.

Look at any of the largest companies in the U.S. right now. If you’re holding a total U.S. stock market index fund right now, you own a meaningful weight in these companies.

For example, as of this recording, owning the total US market means holding over 6% in Apple and just under 6% in Microsoft. Weightings of other top ten companies range from 1% to 5%.

And if you’re globally diversified—as I think you should be—then a market-cap weighted index approach still gives you a nearly 4% weighting in each Apple and Microsoft, with the other top ten company weightings falling between 0.80% and 3.25% each.

In both circumstances, that’s not an insignificant weight and leaves you well positioned to benefit should those companies’ outsized gains continue.

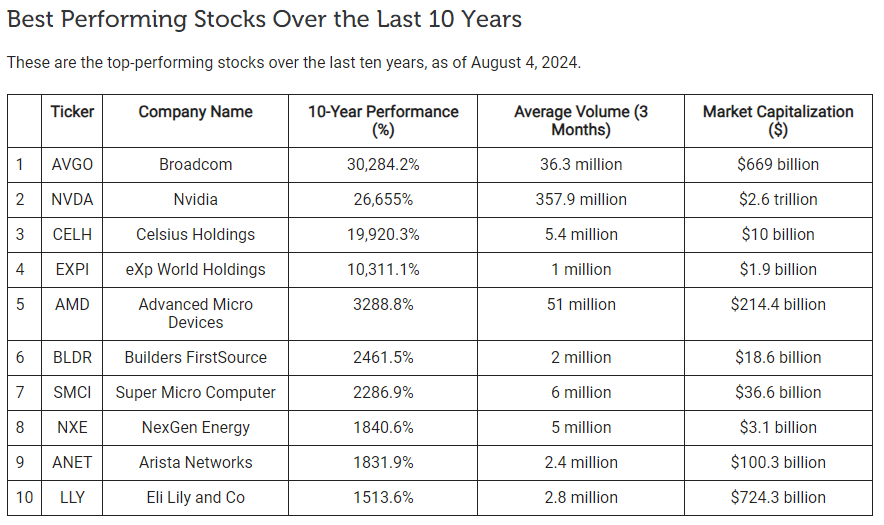

And those are just the biggest companies. Below is a table of the best performing stocks over the last ten years, many of which aren’t mega-cap, household names.

Let me repeat an important statistic from earlier: the top 4% of stocks (1,092 out of 25,967) accounted for all the net wealth creation during that period, with only 90 companies (0.33%) accounting for more than half of the return.

If we know that only a small fraction of companies make up the vast majority of wealth creation in the stock market, you should be less concerned about winning the low probability game of picking those winners in advance and be more concerned with positioning yourself to own the winners no matter what.

Good News: You Owned the Best Performing Stocks All Along

Why do we buy individual stocks?

It’s more tangible. It’s fun and exciting. It gives us a feeling of control over financial outcomes. For some it’s a form of self-expression.

And for many, it’s the result of FOMO because winning investments always find their way to the center of attention. They’re the subject of financial news segments, social media posts, and even conversations with friends or coworkers.

Investing is also highly quantifiable, which can lead us to believe there’s always an objectively optimal decision out there. If we spend enough time thinking or researching or looking, we could find it.

This is largely an illusion, of course; there is no perfect portfolio because we can’t know in advance what investments will win over any given time period. If we kick ourselves for missing an obvious opportunity, it’s probably because we conveniently forgot it was only “obvious” after the fact.

Unfortunately, many people think buying individual stocks is investing. Instead, it’s closer to gambling.

Individual stocks are much riskier than you think. Not only that, picking winners is so difficult that even professional investors whose explicit objective is to do that consistently fail to meet their objective.

When you boil it down to the simplest, first-principle level: the purpose of investing is to grow your wealth at a rate that is greater than inflation without taking undue risk.

When you learn enough about how markets work and the implications the stock market being of complex adaptive systems, it’s all but impossible to see buying individual stocks as something that doesn’t fall into the bucket of undue risk.

And when it comes to growing your wealth at a rate greater than inflation, remember that inflation in the U.S. has historically averaged three percent. Meanwhile, the owning the entire stock market has averaged a return that is roughly 7% above the rate of inflation—isn’t that enough?!?!

No portfolio should exist without a financial plan at its foundation. And no financial plan should require you to find investments that earn a rate of return materially higher than the long-term real return (which is the nominal return minus inflation) of 7%.

It’s really boring advice. So boring, that it’s easy to understand why newspapers don’t plaster that on the front page every day.

Good investing is boring. Good investing is mostly about minimizing mistakes.

When you’re a diversified investor, you can feel pretty confident about two things: (1) you probably won’t miss out on the companies that are driving most of the wealth creation in the stock market, and (2) you are capturing those returns while minimizing the chances of making an unnecessary mistake.

Resources:

- Should You Invest in Individual Stocks?

- Do Stocks Outperform Treasury Bills?

- J.P. Morgan’s Agony and Ecstasy

- SPIVA Scorecard

- Which U.S. Stocks Generated the Highest Long-Term Returns?

- Best Performing U.S. Stocks in the Last Year, 3 Years, 5 Years, and 10 Years

- EP 14: How Markets Work

- EP 70: Thinking of Markets Like Piles of Sand

The Long Term Investor audio is edited by the team at The Podcast Consultant

Submit Your Question For the Podcast

Do you have a financial or investing question you want answered? Submit your question through the “Ask Me Anything” form at the bottom of my podcast page.

Support the Show

Thank you for being a listener to The Long Term Investor Podcast. If you’d like to help spread the word and help other listeners find the show, please click here to leave a review.

I read every single one and appreciate you taking the time to let me know what you think.

Free Financial Assessment

Do you want to make smart decisions with your money? Discover your biggest opportunities in just a few questions with my Financial Wellness Assessment.