Listen Now

How Much Money Do You Need to Retire?

That’s the million-dollar question. Or is it the $2 million question? Maybe it’s $5 million or $10 million.

Regardless, it’s an important question—one that’s also highly personal.

The personal nature of this question is a big reason there aren’t many resources online to help you answer it in a way that feels tailored to your unique circumstances.

While there’s no shortage of articles and podcasts explaining how to save regularly and where to put those savings for growth, the specifics of knowing if you’re on track for retirement often feel elusive.

Even if you’re a high earner maxing out retirement accounts and contributing to taxable investments, you may still wonder if you’re doing enough to replace your income in retirement.

In this episode, I’ll walk you through two different retirement savings benchmarks you can measure your progress against and explain how to apply them to your situation. Then, I’ll share how we answer this question for clients at Plancorp.

Sign up for my newsletter so you can easily reply to my emails with your thoughts or questions for the podcast:

Retirement Savings Benchmarks: Income Multiples

Fidelity’s Savings Guidelines

One of the simplest benchmarks comes from Fidelity, which suggests you should aim to have at least:

- 1x your salary by age 30

- 3x by age 40

- 6x by age 50

- 8x by age 60

- 10x by age 67

The assumptions Fidelity uses to arrive at these benchmarks include:

- An age-based asset allocation similar to Fidelity’s target-date funds.

- A 15% savings rate.

- A 1.5% annual real wage growth rate.

- Retirement lasting from age 67 through age 93.

However, Fidelity also assumes you’ll only need to replace 45% of your pre-retirement income, thanks to factors like Social Security benefits.

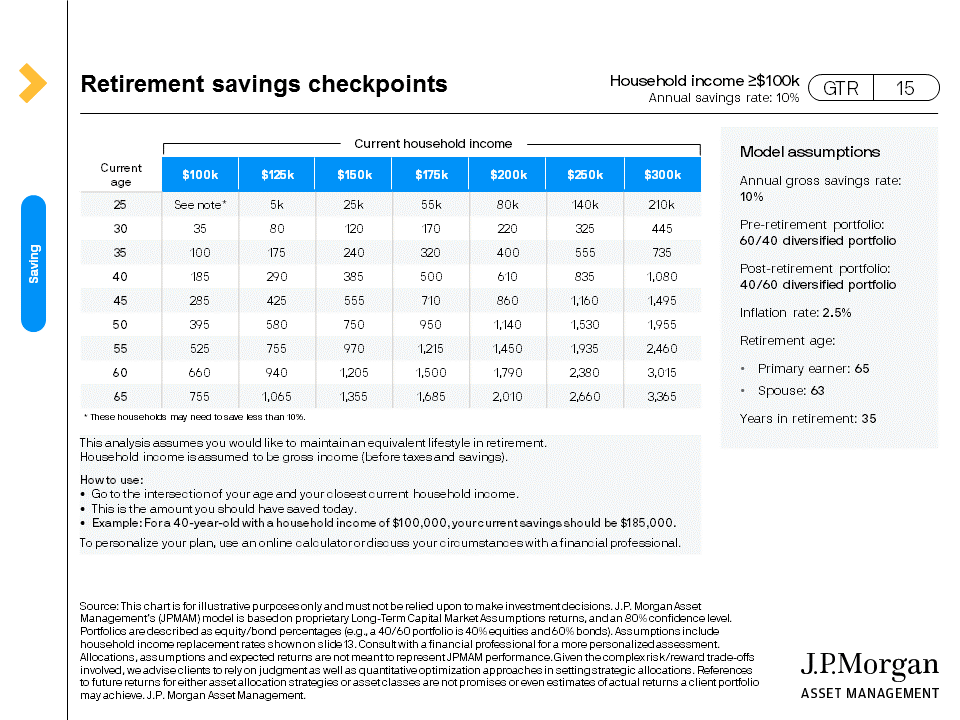

JP Morgan’s Savings Checkpoints

JP Morgan offers an alternative set of income multiples, as illustrated in their Guide to Retirement.

These checkpoints span a range of ages and income levels, making them applicable to more people. JP Morgan assumes:

- A 60/40 portfolio pre-retirement and a 40/60 portfolio post-retirement.

- A 10% savings rate.

- 2.5% inflation.

- A 35-year retirement.

While these benchmarks are easy to use, the assumptions may differ significantly from your personal situation. That’s why it’s important to dig deeper into your specific needs.

Personalizing Retirement Planning: Income Replacement Rates

What Is an Income Replacement Rate?

The next step is determining your income replacement rate—the percentage of your current income you’ll need to replace in retirement.

While a common rule of thumb suggests replacing 75-80% of your income, research highlights a wide range of variability.

For example, a study by David Blanchett, head of retirement research at Morningstar, found income replacement rates ranging from 54% to 87%, with key factors being:

- Pre-retirement income: Higher-income households may need just 60% or less.

- Savings rate: Higher savers require less replacement income.

- Non-portfolio income sources: Pensions, Social Security, or other income streams.

To estimate your replacement rate, subtract the following from your gross income:

- Your annual savings rate.

- Taxes that will decrease in retirement.

- Non-portfolio income (like Social Security).

The result is the income your portfolio needs to replace.

Applying a Withdrawal Rate

Now you can apply a withdrawal rate to come up with a number for how much you need to have saved to comfortably retire.

The most commonly used withdrawal rate is 4%. A few of the underlying assumptions made in the research suggesting a 4% withdrawal rate:

- The 4% spending guideline assumes no variability in lifestyle, which is probably the most unrealistic assumption as retirees spend more in some years and less than others.

- The other big assumptions to know are that the spending rate rises to keep up with inflation.

- The asset allocation is 60% stocks and 40% bonds

- Retirement spans a 30-year time horizon.

Now back to our exercise. Start by multiplying your gross income today by the income-replacement rate you calculated earlier for your portfolio. Then divide that number by the 4% withdrawal rate, which then gives you an estimate for your necessary savings required to retire.

For example, if you have a $250,000 income and assume an 80% income-replacement rate for your portfolio, then you need to withdraw $200,000 a year from your portfolio. Dividing that $200,000 by 4% gives you the estimate of $5 million necessary to retire. If you opted to use a 3% withdrawal rate, the necessary portfolio to support 30 years of your spending jumps to $6.67 million.

For reference, the earlier multiples of earnings from Fidelity assumed that you need $2,500,000 today at age 67 for a 30-year retirement. JP Morgan’s analysis says the need is $3.25 million for a 65-year-old earning the same amount and funding a slightly longer 35-year retirement.

So, as you might expect, retirement benchmarks and rules of thumb result in a wide range of estimates. And that is perhaps why I’m not super comfortable using them in the first place.

Which brings me to the final item I promised at the start of the episode, which is describing the process we use at Plancorp to determine retirement readiness.

The Power of Monte Carlo Simulations

At Plancorp, our process for answering this question relies on Monte Carlo simulations, which run thousands of scenarios to generate a probability that your plan will be successful. Generally speaking, we consider a plan to be “On Track” when 85% of the scenarios provide or exceed the value required to meet all your life goals.

The information that fuels these simulations is gathered through a discovery process where we gather a great deal of personal information on your family make-up, your values, your fears, your interests and hobbies, your personal and professional goals, etc.

Gathering this information allows us to make suggestions as we go through the objective inputs of your plan, which include your: income, cash savings, investments, real estate, any business ownership, your debts, insurance coverage, estate plan, etc.

From there we begin to hone in on the timing and prioritization of your goals. While retirement is the focal point here, it’s rare that people don’t have other objectives beyond their retirement date, and those other goals are important too, so we want to focus on those as well along with the timeline desired for meeting them.

Then we put all those inputs into the Monte Carlo simulation along with our estimates on the potential returns and volatility of your investments, rebalancing parameters, taxes, and inflation.

Once we see the probability of successfully meeting all your goals in that base case scenario, we can start changing inputs to the plan so that you can see how they affect your likelihood of success.

This process translates chances into choices, helping clients see how different variables—like savings rate, retirement age, or spending patterns—affect their financial success.

People are living longer. Healthcare costs are rising. And we have no idea what Social Security will look like in the future. So it’s no surprise that even the best savers have uncertainty around whether they are doing enough.

As you can tell from a few popular retirement benchmarks, answering this question truly depends on your personal situation.

The Bottom Line

While retirement benchmarks offer a helpful starting point, your unique circumstances—such as savings habits, lifestyle goals, and income sources—make personalized planning essential.

If you’re ready to create a retirement plan tailored to your goals, schedule a call with me at www.callwithpeter.com. Let’s build a roadmap that gives you confidence and peace of mind as you approach retirement.

Resources:

- Fidelity Benchmark

- Guide to Retirement by J.P. Morgan

- Estimating the True Cost of Retirement by David Blanchett

- Book a Call with Me

The Long Term Investor audio is edited by the team at The Podcast Consultant

Submit Your Question For the Podcast

Do you have a financial or investing question you want answered? Submit your question through the “Ask Me Anything” form at the bottom of my podcast page.

Support the Show

Thank you for being a listener to The Long Term Investor Podcast. If you’d like to help spread the word and help other listeners find the show, please click here to leave a review.

I read every single one and appreciate you taking the time to let me know what you think.

Free Financial Assessment

Do you want to make smart decisions with your money? Discover your biggest opportunities in just a few questions with my Financial Wellness Assessment.