Listen Now

Welcome back to The Long Term Investor, proud member of the Retirement Podcast Network. Today, we’re diving into a topic that some of you might be facing—or will face soon—what to do when a CD matures.

We’ll explore the factors you should consider, strategies to maximize your earnings, and whether you should renew your CD, move to a high-yield savings account, or even explore higher-risk, higher-reward investments.

Sign up for my newsletter so you can easily reply to my emails with your thoughts or questions for the podcast:

Understanding CD Maturity

As always, I like to start with the basics, which in this case is understanding what it means for a CD to mature.

When you purchase a CD, you’re essentially lending your money to a bank for a set period of time, known as the term. During this term, your money is locked away, earning interest at a fixed rate, which is often higher than what you’d get from a traditional savings account. But, unlike a savings account, the trade-off is that you can’t touch the money without paying a penalty until the term is up.

Now, when we say a CD has “matured,” what we mean is that this term has come to an end. The CD has reached its maturity date, and the bank is now required to return your original deposit along with any interest it has earned over the term.

The bank will typically notify you a few weeks beforehand, either by mail or electronically. This notification is your cue to start thinking about your next move. If you don’t take any action, the bank may automatically roll your funds into a new CD with a similar term, but this new CD may have a different interest rate, and it might not be the best option available to you.

Factors to Consider When Deciding What to Do

This is the moment to consider a few factors…

Current Interest Rates

The first factor to consider is the current interest rate environment. Interest rates fluctuate over time based on economic conditions, and the rate you can get today might be very different from what you locked in when you first opened your CD.

For example, image you’ve been buying 3-month CDs the past year or two since the rates were higher than what you could earn in most bond funds. Perhaps you’ve been earning an annualized rate of 5.09% on those 3-month CDs, which comes out to 1.25% in actual earnings every three months, but the new 3-month CD rate is 4.70% because the Federal Reserve recently telegraphed the start of a rate cutting cycle.

4.70% is still a decent annualized rate, assuming that you can continue to reinvest at that rate 3 months from now, but that isn’t something I would count on with the Fed signaling rate cuts.

See: Should You Hold Cash Instead of Bonds Right Now

In a more normal rate environment, investors earn higher returns for locking in their money for longer periods of time. So if you didn’t have any need for the money, you might consider locking in a longer-term rate, but current market yields are such that short-term rates are higher or similar to long-term rates—a scenario referred to as an inverted yield curve.

Liquidity Needs

Next, let’s talk about liquidity. One of the main downsides of a CD is that your money is locked away for the term, and accessing it early can result in penalties that eat into your earnings. So, when your CD matures, it’s an opportunity to reassess your liquidity needs.

Ask yourself: Do I need access to this money in the near future? Perhaps you have upcoming expenses, like a home renovation, a large purchase, or even a planned vacation. If that’s the case, renewing the CD for another term might not be the best option. You might want to cash out and move the money into a more liquid account, like a high-yield savings account, where you can access it without penalties.

Financial Goals

The most important factor to consider, however, is your broader financial goals. Think about what you want your money to do for you. Are you saving for retirement, building an emergency fund, or setting aside money for a major future purchase?

If the money in question is earmarked for a long-term goal, like retirement, you ought to consider higher-risk, higher-reward options like investments, which we’ll talk more about later.

But if you’re saving for a short-term goal, like buying a car in the next couple of years, a shorter-term CD or a high-yield savings account might be appropriate.

CD Renewal vs. High-Yield Savings Account (HYSA)

Let’s dig in here a little more. Both CDs and HYSAs are low-risk savings vehicles, but they each have their unique advantages and drawbacks. Understanding these can help you choose the option that best aligns with your financial needs and goals.

Should you renew your CD or consider moving your money into a high-yield savings account, often referred to as a HYSA?

CD Renewal

Renewing your CD is a straightforward option, especially if you’re comfortable with the fixed-term commitment and the guaranteed return. When you renew a CD, you’re essentially reinvesting your principal and any earned interest into a new CD, locking in the current interest rate for another term.

Benefits of CD Renewal

- Guaranteed Returns: One of the most appealing aspects of a CD is the certainty it provides. You know exactly how much interest you’ll earn over the term, which can be reassuring in a volatile market.

- FDIC Insurance: Like most savings accounts, CDs are insured by the FDIC up to the maximum allowable limit, making them a very safe place to park your money.

- Higher Rates for Longer Terms: Typically, the longer the CD term, the higher the interest rate. If you don’t need access to your funds for several years, renewing into a long-term CD could offer a better rate than a savings account.

Drawbacks of CD Renewal

- Limited Liquidity: The main downside of a CD is that your money is locked in for the duration of the term. Withdrawing early usually results in penalties, which can negate the interest you’ve earned.

- Fixed Rates: While the stability of a fixed rate is beneficial in a falling interest rate environment, it can be a drawback if rates rise after you renew. You’ll be stuck with the rate you locked in until the CD matures again.

High-Yield Savings Account (HYSA)

On the other side of the coin, a high-yield savings account offers more flexibility while still providing a competitive interest rate. HYSAs have become increasingly popular as they typically offer much higher interest rates than traditional savings accounts, without the long-term commitment of a CD.

Benefits of a HYSA

- Liquidity: Unlike a CD, a HYSA allows you to access your money at any time without penalty. This makes it an excellent option if you need more flexibility or anticipate needing to access your funds.

- Variable Rates: HYSAs typically offer variable interest rates, which means the rate can go up or down over time. In a rising interest rate environment, this can work in your favor as your savings might earn more over time without requiring you to lock in your money.

- Easy Access: With a HYSA, you can usually transfer funds quickly and easily between accounts, making it a convenient option for managing your cash flow.

Drawbacks of a HYSA

- Variable Rates: While variable rates can be a benefit, they can also be a downside if rates drop. Unlike a CD, where your rate is locked in, a HYSA’s rate can fluctuate, potentially lowering your earnings.

- Typically Lower Rates Than CDs: Even though HYSAs offer higher rates than regular savings accounts, they often still fall short of the rates offered by long-term CDs. If your primary goal is to maximize interest and you don’t need immediate access to your funds, a CD might still be the better choice.

When to Choose an HYSA Over a CD?

So, when might it make sense to choose an HYSA over renewing a CD?

Need for Flexibility: If you anticipate needing access to your funds in the near future—whether for an emergency, a planned purchase, or just the peace of mind that comes with liquidity—a HYSA is likely the better option.

Rising Interest Rates: In an environment where interest rates are expected to rise, keeping your money in a HYSA allows you to benefit from those increases without being locked into a lower rate.

Building an Emergency Fund: HYSAs are often the preferred choice for emergency funds due to their combination of higher interest rates and easy access. If your CD has matured and you’re looking to beef up your emergency fund, moving the money to a HYSA could make sense.

Ultimately, the choice between renewing a CD and moving to a HYSA depends on your individual financial goals, your need for access to your funds, and your view on where interest rates might be headed.

Considering Higher-Risk, Higher-Reward Investments

So far, we’ve discussed the options of renewing your CD or moving your money into a high-yield savings account, both of which are low-risk choices. But I think the more interesting consideration is whether you’re willing to take on a bit more risk in exchange for the potential of higher returns?

Generally speaking, I think of CDs as a cash equivalent, so the question becomes should you invest in cash or some mix of stocks and bonds?

Earlier, I noted that the major factors to consider when thinking about what to do when a CD matures were: current interest rates, your liquidity needs, and your financial goals.

When it comes to choosing between cash versus investing in a mix of stocks and bonds, I don’t think you should let current interest rates influence your decision too much. Here’s why:

If the money is intended or needed for long-term goals, we can’t reliably predict future interest rate movements such that we would know the perfect time to get out of cash and into a diversified investment portfolio. That’s simply an acknowledgement that nobody can time the market.

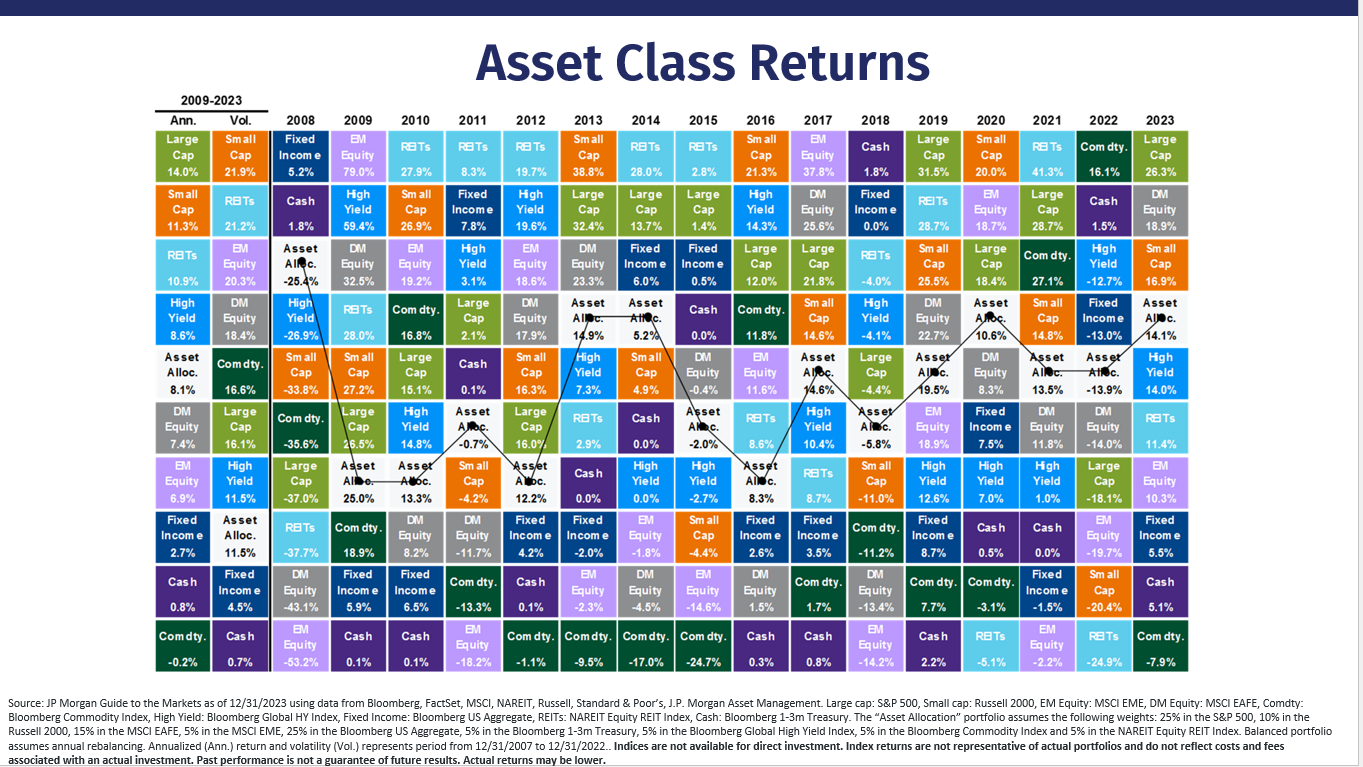

Below is a chart from this quarter’s webinar showing annual asset class returns going back to 2008. Cash is one of those asset classes, and you will see that there are years in which cash is the winning asset class. But like any other equity or fixed income asset class, we can’t know in advance when it will win or lose.

See: Plancorp’s Quarter Market Update Webinar

A diversified portfolio of stocks and bonds will regularly experience bouts of volatility and temporary losses, but those losses and the related uncertainty are the cost of the higher expected returns you earn relative to cash. Losses aren’t the enemy. The need to liquidate during periods of market volatility is.

So if you have a short-term need for the cash, let’s say even something less than five years away, then keeping the maturing CD assets in cash or cash equivalents might make more sense. Personally, I prefer the flexibility of a high-yield savings account, but a CD might be more beneficial if you have perfect foresight into when the money is needed and you can lock in a higher interest rate.

Conclusion

As we wrap up today’s episode, let’s recap what we’ve covered. When a CD matures, you have several options: renewing the CD, moving the funds to a high-yield savings account, or exploring higher-risk, higher-reward investments. Each choice comes with its own set of benefits and drawbacks, and the best option for you will depend on your financial goals, risk tolerance, and time horizon.

Remember, the key is to make an informed decision that aligns with your overall financial strategy. Whether you choose the safety of another CD, the flexibility of a HYSA, or the growth potential of the stock market, it’s all about finding the right balance for your unique situation.

If you found this episode helpful, please leave a review and share it with others who might benefit. And as always, if you have any questions or need further guidance, don’t hesitate to reach out. Until next time, happy investing!

Resources:

- Retirement Podcast Network

- Should You Hold Cash Instead of Bonds Right Now

- Plancorp’s Quarter Market Update Webinar

The Long Term Investor audio is edited by the team at The Podcast Consultant

Submit Your Question For the Podcast

Do you have a financial or investing question you want answered? Submit your question through the “Ask Me Anything” form at the bottom of my podcast page.

Support the Show

Thank you for being a listener to The Long Term Investor Podcast. If you’d like to help spread the word and help other listeners find the show, please click here to leave a review.

I read every single one and appreciate you taking the time to let me know what you think.

Free Financial Assessment

Do you want to make smart decisions with your money? Discover your biggest opportunities in just a few questions with my Financial Wellness Assessment.